Demanding More from Your ASP: Turning Compliance into a Strategic Asset

UAE e-invoicing is mandatory. Your ASP choice is not. The difference between a minimum-viable provider and the right one will show up in your implementation bill, cash flow, and VAT close.

The Decision Most Businesses Are Getting Wrong

By 31 July 2026, every UAE business with annual revenue above AED 50 million must have formally appointed an Accredited Service Provider (ASP) for e-invoicing [1]. Smaller businesses have until March 2027 [1]. The Ministry of Finance (MoF) has published a list of approved providers. The instruction, for most finance teams, sounds straightforward: pick one and move on.

The deadlines are real, the penalties for missing them are AED 5,000 per month [2], and the approved list is right there on the MoF website. But the Ministry itself recognised this is not a simple procurement exercise. In February 2026, alongside its full implementation guidelines, it published a dedicated ASP Selection Guide. The document exists because the regulator understands this is a finance infrastructure decision, not a vendor tick box [3].

There are now over 20 pre-approved providers on that list [4]. Every one has passed the same rigorous accreditation process: Peppol certification, ISO 27001, ISO 22301, minimum two years of e-invoicing operations, UAE data accessibility requirements [4]. The accreditation floor is identical. What happens above it is not. That gap is where the real risk and the real value sit.

How a UAE E-Invoicing ASP Actually Works

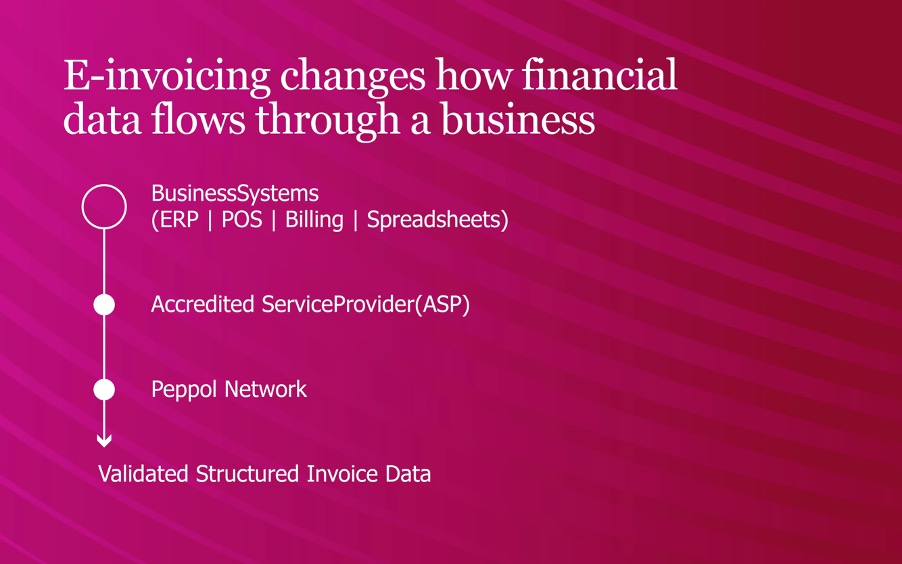

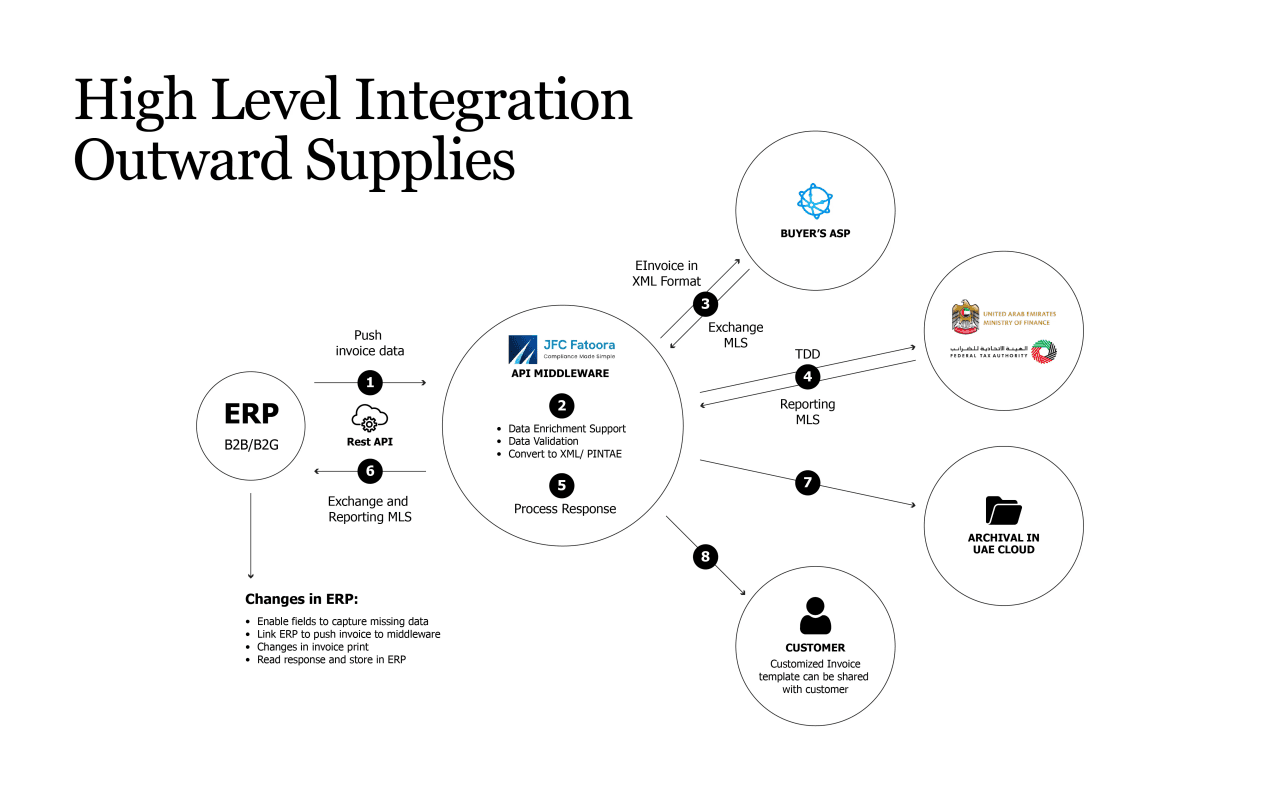

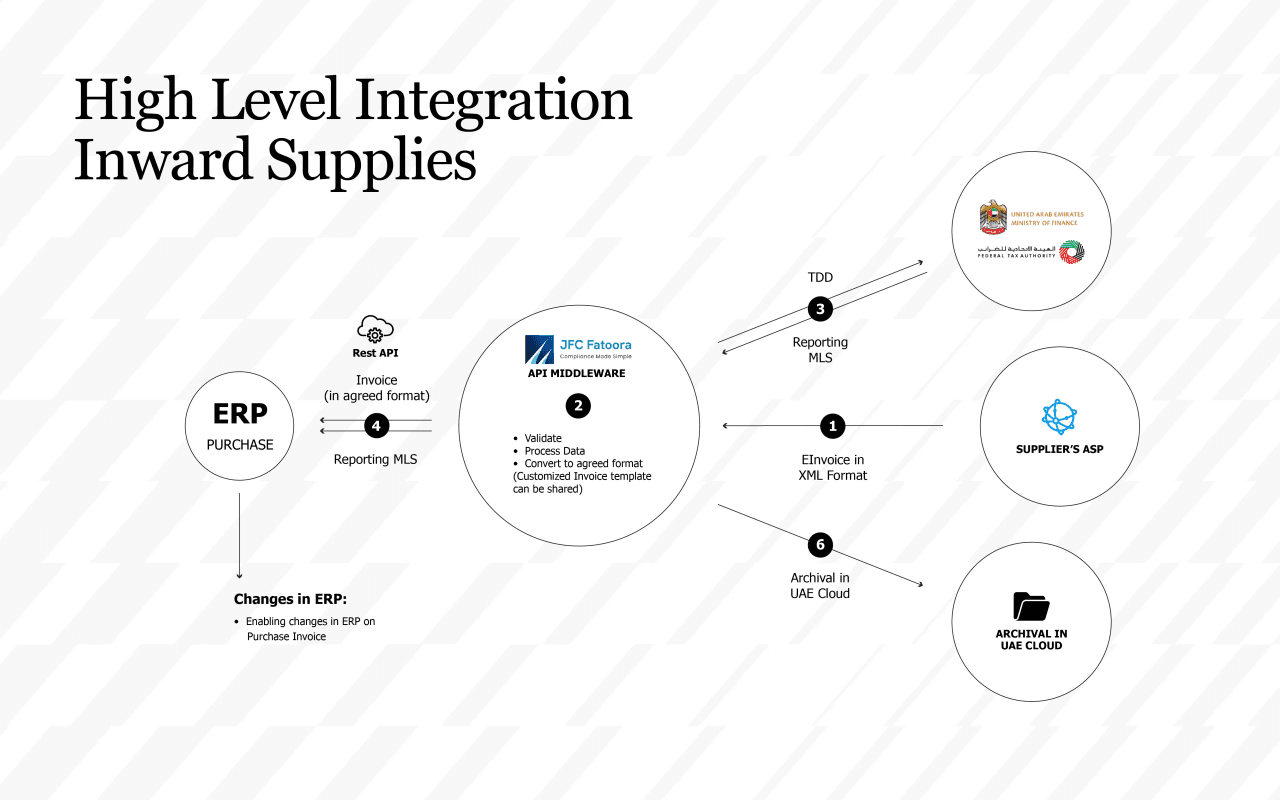

Before evaluating what separates a good ASP from a great one, it helps to understand what the system actually does. The ASP is not optional middleware. It is the only authorised channel between your business and the UAE's e-invoicing infrastructure. Direct connection to the Federal Tax Authority (FTA) is not available to businesses. Every invoice your company sends or receives passes through an accredited provider.

There are two flows to understand.

Outbound (your invoices to customers). Your ERP generates invoice data and sends it to your ASP. The ASP validates that data against the PINT-AE schema, enriches any missing mandatory fields, and transmits the structured XML invoice through the Peppol network to your customer's ASP. The customer's ASP validates from their side and delivers the invoice into the buyer's system. Simultaneously, both ASPs report the relevant tax data to the FTA. The FTA acknowledges receipt, and that confirmation travels back to you. Your ERP reflects the outcome (accepted, delivered, or rejected) without your finance team touching a portal.

Inbound (invoices from suppliers). Your supplier's ASP routes the invoice via Peppol to your ASP. Your ASP validates it, converts it to whatever format your ERP or AP system expects, and delivers it into your accounts payable workflow. Your ASP also reports the tax data to the FTA on your side. What arrives is a structured, validated invoice, not a PDF in an inbox, not a file to manually key in.

Changing providers later means re-integrating, re-testing, and potentially disrupting live invoice flows. You will live with this choice for years.

What Every ASP Must Do — And Why That Is Not Enough

The MoF accreditation requirements define a precise compliance floor. Every pre-approved ASP validates invoices against the PINT-AE schema (Peppol International Invoice for UAE, with 51 mandatory fields) [5], routes them through the Peppol 5-corner network, reports tax data to the FTA in near-real time, delivers message-level status confirmations, assigns unique identifiers to every invoice, and maintains records accessible to the FTA on request [3]. None of this is optional, and none of it separates one provider from another.

Think of it in four layers:

- Layer 1 (compliance floor): The mandated baseline above: every accredited ASP delivers this.

- Layer 2 (table stakes): Native ERP connectors for SAP, Oracle, Dynamics, and Zoho; real-time invoice status sync back into the ERP; structured exception handling when invoices fail.

- Layer 3 (strategic differentiators): Working capital intelligence, VAT reconciliation automation, cross-border interoperability, AI-powered anomaly detection, regulatory update absorption.

- Layer 4 (forward-looking): Dynamic discounting, supply chain finance, readiness for when the mandate extends to B2C.

Most ASP conversations stop at layer two. The selection decisions that matter start at layer three.

The Real Cost of UAE E-Invoicing Implementation

The cost of e-invoicing implementation is not a reason to delay. The penalties for missing deadlines make that clear. But it is a serious reason to choose carefully the first time.

Implementation costs vary significantly by business complexity. Setup runs between AED 50,000 and AED 500,000. Full enterprise implementation (ERP integration, API development, sandbox testing, training, and hypercare) typically lands between AED 575,000 and AED 1.45 million, with payback expected over 12 to 24 months [6]. That range is wide, and where a business ends up within it depends heavily on how well its ERP and master data are prepared before onboarding begins. Messy data and an unprepared ERP do not just slow implementation. They multiply the billable hours.

Against those costs, the MoF projects that e-invoicing will reduce invoice processing costs by 66–80% [7]. For a business processing 5,000 invoices per month, independent estimates put the annual operational saving at AED 220,000 to AED 510,000 [8]. The difference between the low and high end of that range is not invoice volume. It is ASP capability and integration quality. A well-integrated ASP that automates AP and AR workflows, eliminates manual reconciliation, and feeds clean data into VAT return preparation recovers substantially more value than one that routes invoices and stops there.

Penalty exposure compounds this. At AED 100 per rejected invoice with a monthly ceiling of AED 5,000 [2], even a 2–3% rejection rate at volume generates a persistent drain. The AED 1,000 per day fine for failing to notify the FTA of a system outage [2] adds another tail risk, one that falls on the business whether the failure originated with the ASP or internally.

Then there is the switching cost argument, which rarely surfaces in implementation planning. Changing ASP after go-live means re-doing the full integration cycle: new API development, new sandbox testing, re-mapping of ERP fields, potential re-onboarding of trading partners, and a compliance exposure window during transition. The businesses that pay for a gap assessment twice are the ones that skipped it the first time.

Three Mistakes UAE Businesses Make When Choosing an ASP

Choosing on speed rather than fit. The July 2026 deadline for Phase 1 businesses creates pressure to sign quickly. A typical ASP onboarding runs four to six months from contract to go-live [6], covering API integration, ERP configuration, master data mapping, sandbox testing, and training. The real risk is not signing too late. It is signing too fast with a provider whose capabilities do not match your operational complexity, and discovering this six months in when switching is expensive.

Evaluating the ASP without evaluating the ERP. An ASP sits between your ERP and the FTA. When an invoice is rejected (at AED 100 per incident [2]), the problem is usually not the ASP. It is dirty master data: an incorrect TRN, a missing buyer Peppol participant ID, a misconfigured tax classification for a free zone supply. The ASP cannot fix data problems it did not create. Businesses that treat ASP selection as separate from their ERP state are preparing for a difficult go-live.

Letting IT own the decision. The best ASPs do things that matter deeply to a CFO and barely register in an IT evaluation. The MoF confirmed that structured e-invoice data will pre-populate VAT return fields and speed up refund processing [7]. A well-chosen ASP reduces the quarterly close burden, automates ERP-to-FTA reconciliation, and surfaces receivables data in near real time. These capabilities are invisible in a feature spreadsheet. They show up in DSO, in close time, and in how your team spends the last week of every VAT period.

What Best-in-Class ASPs Deliver Beyond the Mandate

Working capital and cash flow. Near-real-time AR visibility from structured XML data means the receivables picture does not depend on a month-end close. The MoF was direct about this: e-invoicing creates conditions for faster payment and better working capital management [7]. Better providers surface DSO trends, flag overdue patterns, and in some cases connect to dynamic discounting programmes where suppliers offer early payment terms in exchange for accelerated cash [7]. Finance teams rarely ask for this in an ASP RFP. It tends to be the feature that makes a contract worth renewing.

Tax compliance efficiency. When invoice data flows cleanly from ERP through ASP to FTA, the records feeding a VAT return already exist in the format the FTA expects. Providers that automate reconciliation between ERP-reported and FTA-submitted figures eliminate a manual process most finance teams currently run over two to three days at quarter end. That is not a technology improvement. It is time returned to work that requires judgement.

Operational resilience and future reach. The UAE's system runs on Peppol, the same framework used in Saudi Arabia, Singapore, and across Europe. An ASP already operating across those jurisdictions routes cross-border invoices natively, without format conversion or a second vendor relationship. Better providers also absorb MoF schema updates internally; when the PINT-AE data dictionary changes, it lands in the ASP's validation engine, not your IT backlog. Providers with AI-powered anomaly detection catch duplicate invoices, suspicious vendor patterns, and data inconsistencies before transmission, not during an FTA audit.

Three ASP Models — And Which One Fits Your Business

Not all ASPs are the same kind of company. This distinction matters as much as the feature comparison.

Tech-first platforms are automated, scalable, and low-touch. Broad ERP connector libraries, usage-based pricing, self-service onboarding. The right choice for a business with a capable internal finance and IT function, clean ERP data, and primarily domestic invoice flows. They provide a reliable pipe, not a partner.

Advisory-led ASPs bring tax, compliance, and ERP expertise into the engagement alongside the platform. The relationship includes guidance on VAT return implications, Corporate Tax treatment, and FTA audit preparedness, not just system configuration. For businesses still building their finance infrastructure, or where the compliance picture is complex (free zone supplies, VAT group structures, reverse charge, intercompany billing), this model reduces the risk of getting the implementation technically correct while being commercially wrong.

Globally-present ASPs with regional depth are already running in production across multiple Peppol jurisdictions. Saudi Arabia's Fatoora system has been live since 2021, drawing in progressively smaller taxpayers through successive integration waves [9]. Providers that have operated through those waves alongside UAE-based clients running dual-jurisdiction know the operational detail that does not appear in compliance documentation. For any business with KSA operations, a GCC supply chain, or a multinational parent managing group-wide e-invoicing policy, a single ASP handling cross-border flows without separate vendor contracts is a concrete advantage.

The right model depends on your internal finance capability, your compliance complexity, and your geographic footprint. That is exactly what a gap assessment establishes before you go to market.

Why an E-Invoicing Gap Assessment Comes Before the RFP

Most businesses issue an RFP before they know what they actually need. The RFP describes the mandate requirements, asks providers to confirm accreditation, and requests pricing. It does not surface the issues that will determine whether the implementation works.

A structured, expert-led gap assessment covers the ground the RFP misses: ERP readiness and e-invoicing ERP integration architecture, master data quality (TRN accuracy, buyer Peppol participant IDs, tax classifications), VAT compliance position across all entities and transaction types, free zone and VAT group treatment, and cross-border invoice flows already in operation. It also maps current reconciliation processes against what automated reconciliation would require, surfacing the manual workarounds that ASP onboarding will expose. Formal ASP appointment is completed through the FTA's EmaraTax portal, but the preparation that makes that onboarding succeed happens well before you log in.

The output is not a vendor shortlist. It is a requirements specification in finance terms: which ASP model fits, which integration approach is realistic given your ERP state, and what needs fixing internally before any provider can do their job properly. Businesses that skip this step tend to pick the ASP that presents best, onboard it against an ERP that was not ready, spend months troubleshooting rejections, and eventually pay for the assessment they should have done first.

Five questions worth putting to any shortlisted provider:

- What does your onboarding process do to our ERP master data before go-live?

- How does your platform connect invoice data to our VAT return preparation?

- When the MoF updates the PINT-AE schema, who absorbs that change, how fast, and does it require anything from our side?

- If we operate in KSA, hold a VAT group structure, or expand regionally, how does your platform handle that natively?

- What was your rejection rate in sandbox testing, and what is your exception management process once we are live?

The answers will tell you more about fit than any feature matrix.

Every ASP on the MoF list will keep you compliant. Only some of them will make your finance team's life meaningfully better. That distinction is worth two weeks of evaluation time.

Sources

1. Ministerial Decision No. 244 of 2025 on the Implementation of the Electronic Invoicing System — UAE Ministry of Finance (September 2025). https://mof.gov.ae/wp-content/uploads/2025/09/Ministerial-Decision-No.-244-of-2025-on-the-Implementation-of-the-Electronic-Invoicing-System.pdf

2. Cabinet Decision No. 106 of 2025 on Violations and Administrative Penalties — UAE Ministry of Finance (2025). https://mof.gov.ae

3. UAE Electronic Invoicing Guidelines V1.0 — UAE Ministry of Finance (February 2026). https://mof.gov.ae/wp-content/uploads/2026/02/UAE-Electronic-Invoicing-Guidelines_V-1.0-23Feb2026.pdf

4. Pre-Approved eInvoicing Service Providers — UAE Ministry of Finance (updated periodically). https://mof.gov.ae/en/about-ministry/mof-initiatives/einvoicing/pre-approved-einvoicing-service-providers/

5. UAE: Technical Guidance on Mandatory E-Invoicing Fields — KPMG UAE (February 2026). https://kpmg.com/us/en/taxnewsflash/news/2026/02/uae-technical-guidance-mandatory-e-invoicing-fields.html

6. Accredited Service Providers in UAE E-Invoicing: Role, Selection and Onboarding — Rockford Computer (February 2026). https://rockfordcomputer.ae/accredited-service-providers-asps-in-uae-e-invoicing-role-selection-onboarding/

7. eInvoicing — UAE Ministry of Finance (2025). https://mof.gov.ae/en/about-ministry/mof-initiatives/einvoicing/

8. Navigating E-Invoicing in the UAE: A Step-by-Step Guide — Fiscal Requirements (2025). https://www.fiscal-requirements.com/news/4802

9. UAE E-Invoicing Mandate 2026: Readiness, ASP, and PINT AE — Avalara (March 2026). https://www.avalara.com/blog/en/europe/2026/03/uae-e-invoicing-mandate-2026-readiness-asp-pint-ae.html

Ready to Start with the Assessment, Not the RFP?

Finline helps UAE businesses understand exactly what they need from an ASP before they go to market.