When Does a UAE Business Actually Need a CFO?

Most UAE businesses ask which CFO model to use before deciding whether they need CFO-level oversight at all. A practical guide to financial leadership, the FTA relationship, and the right engagement model for your stage.

When Does a Business Need CFO-Level Oversight?

For most UAE businesses, the CFO question arrives in the wrong order. They ask which model to use before they have decided whether they need CFO-level financial oversight at all. That distinction matters, and getting the structure wrong is more consequential now than it was a few years ago, for reasons specific to the regulatory environment the UAE has built.

A bookkeeper records what happened. An accountant ensures those records are accurate at the transaction level. A CFO, or someone operating at that level, looks forward: financial structure, regulatory positioning, relationships with banks and investors, and the decisions that sit above the numbers rather than inside them.

For many businesses, the gap between those two jobs stays invisible until something forces it into view. The practical signals that a finance function has been outgrown tend to look like this:

Corporate tax is no longer straightforward. You have more than one entity, intercompany transactions, or free zone and mainland operations running in parallel. Filing is no longer a form to complete. It requires judgment about positions, documentation standards, and the timing of elections. Under the Corporate Tax Law (Federal Decree-Law No. 47 of 2022), businesses with related-party transactions must apply the arm's length principle and, depending on threshold, maintain Transfer Pricing documentation under Ministerial Decision No. 97 of 2023.

The FTA has been in contact, or is likely to be. An inspection visit, a request for records, a VAT audit, or a need to file a voluntary disclosure. Each of these requires someone who understands both the regulatory framework and how your numbers were constructed, and who can manage the correspondence with the authority on your behalf.

A bank, investor, or counterparty is asking financial questions. Covenant reporting, due diligence, financial projections presented at board level. These require a finance function that produces credible, structured outputs on demand, not reports built from scratch when someone asks.

The business is growing faster than the finance function can track. Cash flow surprises you. Margins are less clear than they should be. Decisions are being made on bank balances rather than managed numbers.

None of these situations requires a full-time CFO as the first response. They require CFO-level thinking. The question of which engagement model delivers that is separate.

The FTA and MoF Relationship: What It Actually Requires

The Federal Tax Authority administers corporate tax alongside VAT and excise. The Ministry of Finance sits above it as the policy and legislative authority, issuing ministerial decisions and cabinet resolutions that businesses are expected to apply correctly from their effective date. The relationship between a UAE business and these two bodies is now more active than most businesses anticipated when corporate tax was introduced.

The FTA's market inspection activity has grown substantially. The Authority conducted 176,000 market inspection visits in 2025, up 89% on the previous year, as reported by the FTA directly [1]. These visits aim to ensure taxpayers comply with tax laws, including the correct issuance of tax invoices and payment of taxes due. They are not announced in advance, and a business that has been filing without CFO-level review is more likely to have accumulated inconsistencies that attract that attention.

When an inspection or audit takes place, the business needs to produce records, reconcile positions, and respond to queries within defined timeframes. Under the Tax Procedures Law (Federal Decree-Law No. 28 of 2022), the FTA has broad powers to request information and documentation. Responding to that process requires someone who understands the filing positions taken, can explain them clearly, and can manage the exchange with the authority. A bookkeeper or junior accountant is not structured for that role.

The voluntary disclosure mechanism exists for a reason. If an error in a previous return is identified, the Tax Procedures Law provides a route to correct it, and the timing and manner of that disclosure affects the outcome. CFO-level oversight means errors are more likely to be caught and addressed before the FTA identifies them, which is the preferable position to be in.

The MoF also issues decisions that change compliance requirements with limited lead time. E-invoicing is the most immediate example. Under Ministerial Decisions 243 and 244 of 2025, businesses with annual revenue below AED 50 million must appoint an accredited service provider by 31 March 2027 and implement the electronic invoicing system from 1 July 2027 [2]. The MoF has confirmed that unstructured formats including PDF, Word, scanned copies, and emails do not constitute electronic invoices under this framework [3]. Non-compliance carries penalties under Cabinet Decision No. 106 of 2025, including AED 5,000 per month for failing to implement the system or appoint an accredited provider [4]. Assessing what this requires, updating systems, and appointing the right provider is a finance leadership task, not an accounting one.

Managing the FTA and MoF relationship is not a compliance task. It is a financial leadership task.

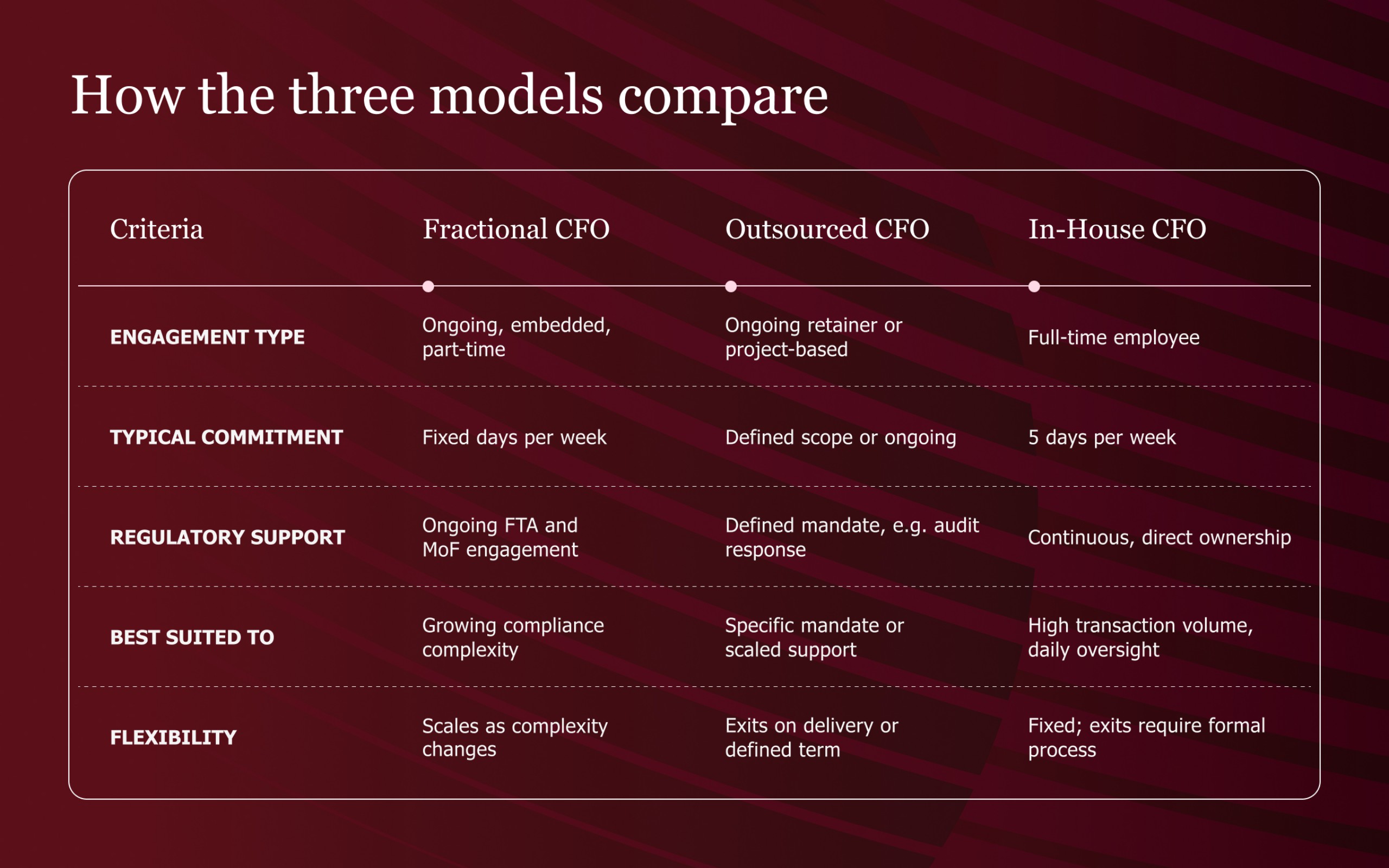

The Models Available

Once it is clear that CFO-level oversight is needed, the question is which engagement model provides it. The UAE market uses several terms, often interchangeably. The structural differences are real.

Fractional CFO. Ongoing and embedded. Works part-time across your business, typically a fixed number of days per week. Attends leadership meetings, owns the financial planning and forecasting cycle, and maintains continuity between sessions. Has other clients, but yours are a standing commitment. This is the closest external equivalent to a full-time internal CFO: same strategic function, different employment structure.

Outsourced CFO. Can describe the same thing as fractional, an ongoing retained engagement with regular cadence and strategic ownership. Or it can mean something project-based: a defined mandate, a scope, and a close date. Fundraising preparation, FTA audit response, systems implementation, due diligence support. The work ends when the deliverable lands. The distinction matters because the cost, the depth of involvement, and the expectations differ depending on which structure you are actually engaging.

In-House CFO. Full-time employee. Daily presence. Carries full employment costs: base salary, housing allowance, visa, medical insurance, gratuity, performance bonus. The right answer when transaction complexity, entity count, or capital activity genuinely requires someone available every day.

None of these is inherently better. The right model depends on what the business needs the finance function to do.

Choosing the Right Model

Revenue is a starting point, not the whole answer. A business at a given revenue with a single entity and no related-party transactions has different CFO requirements than one at the same revenue managing a free zone holding structure, a mainland operating entity, and intercompany service agreements. What matters is the complexity of the compliance picture and how actively that picture needs financial leadership to manage.

An ongoing fractional or retained outsourced model is typically right when corporate tax is a live obligation with more than one entity or meaningful related-party activity, and the person currently managing your finance function is not equipped to handle FTA correspondence, prepare Transfer Pricing documentation under Ministerial Decision No. 97 of 2023, or model your tax position for the year ahead. This describes most UAE businesses in the growth phase, where the compliance stack has become more demanding than the finance function was built to handle.

Businesses electing for Small Business Relief under Article 21 of the Corporate Tax Law and Ministerial Decision No. 73 of 2023 are not required to maintain Transfer Pricing documentation while that relief applies, though they must still apply the arm's length principle. Two things end the relief: revenue exceeding AED 3 million in a Tax Period, or the scheme's own expiry, since Small Business Relief is only available for tax periods ending on or before 31 December 2026. Once it lapses, those documentation obligations apply from that point [5]. That transition requires a finance function prepared to take them on.

A project-based outsourced engagement fits a defined task with a clear deliverable: preparing for an FTA inspection, building investor-ready financial models, implementing a new finance system, or responding to a specific regulatory query. The engagement has a scope and closes on completion. An ongoing retainer may follow, or it may not.

An in-house CFO becomes the right answer when the business consistently generates the transaction volume and entity complexity that requires daily financial oversight. When multi-entity reporting, bank relationship management, and board-level financial communication all need to happen continuously, a full-time seat is justified.

The Cost Question

Most businesses benchmark against the full-time CFO when evaluating alternatives. An experienced senior finance executive in the UAE carries a substantial employment cost once housing, medical, visa, gratuity, and bonus are included alongside base salary. For many businesses in the growth phase, that total cost is disproportionate to what the role would need to deliver day-to-day.

Outsourced and fractional models cost less, though how much less depends on the engagement structure, the scope, and the seniority of the person involved. The relevant comparison is not just the fee against the salary. It is what each model actually delivers against what the business needs the finance function to do.

The more useful framing is what the absence of financial leadership costs. An incorrectly filed corporate tax return, a related-party transaction without proper documentation, a VAT position that needs retrospective correction. These create costs that are not always visible until they materialise. Under the administrative penalties framework, failing to register for corporate tax by the applicable deadline carries an AED 10,000 penalty per the FTA's published guidance [6]. Failing to implement the electronic invoicing system or appoint an accredited provider within the required timeframe carries AED 5,000 per month under Cabinet Decision No. 106 of 2025 [4].

The cost of the wrong hire, at any seniority, is also real. A profile suited to a much larger business is not the right profile at the current stage, and the mismatch creates its own costs. The right structure is the one proportionate to what the business needs now, with enough flexibility to change as the regulatory and operational picture develops.

Sources

1. Federal Tax Authority. "FTA Conducts 176,000 Market Inspection Visits in 2025, an 89% Year-on-Year Increase." tax.gov.ae (2026). https://tax.gov.ae/en/media.centre/news/

2. UAE Ministry of Finance. Ministerial Decisions No. 243 and 244 of 2025 on the scope and timelines for implementing the Electronic Invoicing System. mof.gov.ae (2025). https://mof.gov.ae/en/news/ministry-of-finance-announces-targeted-amendments-to-einvoicing-system-decisions/

3. UAE Ministry of Finance. eInvoicing Programme overview: unstructured formats (PDF, Word, scanned copies, emails) are not valid electronic invoices. mof.gov.ae (2025). https://mof.gov.ae/en/about-us/initiatives/einvoicing/

4. UAE Cabinet Decision No. 106 of 2025 on Violations and Administrative Penalties for the Electronic Invoicing System. mof.gov.ae (2025). https://mof.gov.ae/en/about-us/initiatives/einvoicing/

5. Federal Tax Authority. Small Business Relief Guide (CTGSBR1), Article 21 of the Corporate Tax Law and Ministerial Decision No. 73 of 2023. tax.gov.ae (2023). https://tax.gov.ae/Datafolder/Files/Guides/CT/Small%20Business%20Relief%20Guide%20-%20EN%20-%2029%2008%202023.pdf

6. Federal Tax Authority. Corporate Tax late-registration penalty of AED 10,000 (Cabinet Decision No. 75 of 2023). tax.gov.ae (2025). https://tax.gov.ae/en/about.fta/waiver.of.penalties.aspx

Not Sure Which CFO Model Your Business Needs?

Talk to our team about structuring CFO-level financial oversight around your current stage, your compliance obligations, and your relationship with the FTA.